The Anatomy of a Fund Universe

There are eleven types of mutual fund: knowing them will help you find the good and avoid the bad.

Spend time studying funds, and you’ll begin to recognise “types” that crop up over and over again. Get to know these types (there are eleven of them) and you’re on your way to understanding which funds to hold, and which to avoid like the plague.

I originally identified these when compiling the “State of the Universe” report in 2012. To write that report, I went deep-geek into the fund world, highlighting how the often-heard term “the average fund” confuses matters (because very few funds in any given sector look anything like average).

Ten years, and a lot of water under the bridge, later. I thought I’d revisit them. Turns out they’ve stood up well, so I’m polishing them and uploading them here. I hope they help.

The Anatomy of a Universe: The Eleven Types of Fund

Key: What are the Eleven Types of Funds?

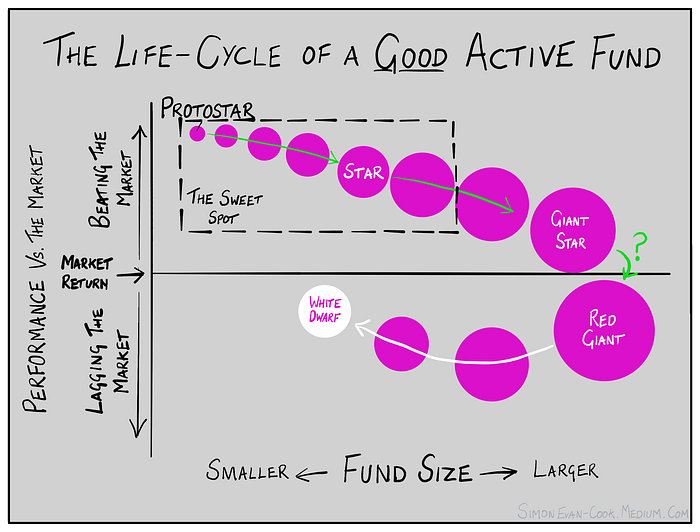

Protostar

This is a relatively small, possibly young, actively-managed fund that has outperformed the market by a long way. It has done so because its manager is skillful, and has an edge over the market that can be repeated.

Star

This is a protostar (or possibly a shooting star) that has grown bigger on the back of previous good performance. Large funds are harder to manage than smaller funds, so it’s unlikely to outperform by as much now, but it’s still small enough to keep winning.

Giant Star

A star that has continued to perform well, making it more popular, which attracted further inflows, which had made it even bigger. It’s very difficult for a fund this large to keep outperforming, but the manager may be unusually talented, and have a style that works well at scale. But if the fund isn’t closed to new flows soon, it risks becoming a Red Giant. Given its size, it will have an outsize impact on whether fund investors — on average — gain value from active management in the coming years (but will have very little impact on how the “average” fund performs, as that calculation usually ignores fund size).

Red Giant

An active fund that has grown very large on the back of previous good performance, but is now struggling to beat its market. This suggests it’s beyond the peak of its life cycle. When a fund gets this big, the manager can no longer invest in the same way as when it was enjoying its earlier stellar run, so we shouldn’t expect the same performance.

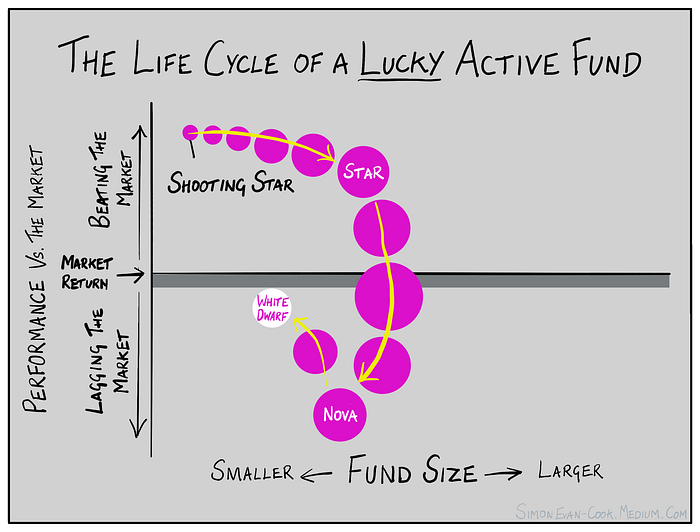

Shooting Star

This sits in the same part of the universe as a protostar. It’s a small, actively-managed fund that has beaten its market by a long way. However, unlike a protostar, this was due to luck, not repeatable skill. So despite going on to look — briefly — like a star, it’s nothing of the sort. It will soon flare out before disintegrating.

Nova / Supernova

A fund that is undergoing a spectacular collapse. Having previously been a star (or a giant star in the case of a Supernova), it attracted a lot of investors’ money on the back of strong performance. But now, for whatever reason, that performance has reversed. So its holders are pulling money out, which loads additional pressure onto the fund, its manager, and the fund management company.

White Dwarf

Basically a dead fund. This may have been a star, or a giant star, that died spectacularly, becoming a nova/supernova as it did so. Now all that’s left is the money of holders who are hoping for a “rebound”. Or who have forgotten they owned it. Or are stuck in it (because the collapse led to the fund having to close its doors to redemptions). It’s likely that, having been through this cycle, it is no longer run as it was when it was in its growth phase, so it looks more like a black hole than the star it was in its prime.

Black Hole

A fund that’s marketed better than it’s managed. The company that owns it probably has powerful distribution channels, filled with clients who don’t know any better. The fund is described as “active”, but the manager is basically copying the market and charging for it. Its unspoken aim is to never be far enough behind the market to raise alarm, which usually means it’ll never be far enough ahead of the market to justify its fees (more commonly known as a closet tracker).

The Tracker Belt

The band just beneath the market’s return where most trackers should sit. Trackers openly copy the market. The largest of them are likely to have the lowest charges in their sector. Many people believe this makes it a mathematical fact that they will outperform the “average” fund in their sector.* But many people also believe it’s acceptable for a grown-up to wear Crocs in public: Doesn’t make it true.

Planets

Average to small-sized funds that, because of patchy, lukewarm performance, will probably remain that way. Most planets are likely to underperform over a market cycle due to the impact of fees and/or poor decision making. (NB The quality of planets has, in my opinion, risen over the last ten years, as their fees have fallen and the weakest have been driven out by competition from low-cost trackers).

Matter

Small funds that come and go (‘matter’ is an ironic name given that, in the grand scheme of things, most of them don’t). Most matter have the following life cycle: Get launched, attract little money, underperform, get shut down. However, it is from matter that tomorrow’s protostars and stars will emerge, so it plays an important, but overlooked role, in keeping the industry healthy and competitive (remember that Vanguard’s behemoth S&P 500 tracker, which has revolutionised the entire industry, once floated among the matter). Sadly, despite being basically harmless, there is a growing view within the UK’s fund industry that matter is little more than an annoyance, and should therefore be squeezed out of existence.

Just a Theory?

To give this a bit of real-life credibility, here’s a look at the UK’s universe of global equity funds (The IA Global Sector). It fits pretty well, I’d say. In my experience, most sectors look something like this:

Now, I could label this up; tell you which fund is which “type” and all that. But I’m shorter on time than I was in 2012, so you’ll have to work that out for yourselves. Besides, you’ll learn more that way — I certainly did.

Finally then, just as in 2012, I’ll point out what I think should be the aim of any fund picker. Or any fund picker that’s aiming to run something other than a funds-based version of a Black Hole, anyway. (You know who you are).

We should seek out protostars, then hold onto them for as long as they look capable of remaining a star. This is the sweet spot; where the best performance is to be had (and not among the Giant Stars and Red Giants that everyone else is buying).

The rub, though, is that protostars live in the same part of the universe as Shooting Stars: funds which look great, but have just been lucky. It’s all too easy to mistake one for the other. Buying a Shooting Star will damage your wealth (or, if you’re a professional, your career). So, if you don’t know what you’re doing, it’s riskier than following the herd into a Giant Star or a Tracker. (But if you’re a professional, you’re paid to know what you’re doing. So what’s stopping you?)

How can we reduce that risk?

Study history. Work out what was repeatable, and work out what wasn’t. What separated the good from the lucky? And once you’ve done that, buy lots of the former, and none of the latter.

This means that constructing a winning portfolio of funds is — as the saying goes — simple, but not easy.

Footnotes

*I’m not getting into this here (because I get into it everywhere else, all the time), but what they actually mean is “the average pound/dollar/dong/whatever invested in a market can’t outperform the market”. That’s the mathematical fact. Although given the complexity of it all, there may well be some real-life rinky dink that means that’s not actually true either.